Private Letter Rulings - Pet Therapy Organization Denied Exemption

GiftLaw Note:

Several years ago D founded a sole proprietorship to provide healing sessions for animals in distress. While D worked with animal rescues, she also held private healing sessions with clients for a fee. However, D operated the sole proprietorship at a loss. Because opportunities arose to receive donations and sponsorships, D founded Org as a Sec. 501(c)(3) non-profit corporation to provide the same services as the sole proprietorship. These services include retreats, sessions for individuals and their pets for a suggested donation similar to the fee the sole proprietorship charged and workshops and seminars for a fee. All of these services will be provided by D who is also Org’s President, Executive Director and only employee. Org will also advertise itself using the same website that D’s sole proprietorship used.

Section 501(c)(3) of the Code states that an organization will be exempt from income tax if it is organized and operated exclusively for one or more exempt purposes. Here, the Service found that Org failed the operational test because it was operating for the benefit of its founder, D. D only created Org because her sole proprietorship was operating at a loss. To that end, Org performs the same services as the predecessor sole proprietorship. D is the founder, executive director, president and only paid employee of Org and has complete control of its operations. Org’s website also links to a for-profit jewelry business D operates. Based on the above, the Service found Org was operated in a manner similar to D’s sole proprietorship and other commercial enterprises. Therefore, the Service denied Org’s application for exemption.

Section 501(c)(3) of the Code states that an organization will be exempt from income tax if it is organized and operated exclusively for one or more exempt purposes. Here, the Service found that Org failed the operational test because it was operating for the benefit of its founder, D. D only created Org because her sole proprietorship was operating at a loss. To that end, Org performs the same services as the predecessor sole proprietorship. D is the founder, executive director, president and only paid employee of Org and has complete control of its operations. Org’s website also links to a for-profit jewelry business D operates. Based on the above, the Service found Org was operated in a manner similar to D’s sole proprietorship and other commercial enterprises. Therefore, the Service denied Org’s application for exemption.

10/2/2015 (7/1/2015)

Dear * * *:

This is a final adverse determination regarding your exempt status under section 501(c)(3) of the Internal Revenue Code (the "Code"). It is determined that you do not qualify as exempt from Federal income tax under section 501(c)(3) of the Code.

Our adverse determination was made for the following reason(s):

You have not demonstrated that you are operated exclusively for exempt purposes within the meaning of Internal Revenue Code § 501(c)(3) and Treasury Regulations § 1.501(c)(3)-1(d), in that you have failed to establish that your substantial activity of pet/owner healing for a fee has an exempt purpose.

Contributions to your organization are not deductible under section 170 of the Code.

You are required to file Federal income tax returns on Forms 1120. File your return with the appropriate Internal Revenue Service Center per the instructions of the return. For further instructions, forms, and information please visit www.irs.gov.

If you were a private foundation as of the effective date of the adverse determination, you are considered to be taxable private foundation until you terminate your private foundation status under section 507 of the Code. In addition to your income tax return, you must also continue to file Form 990-PF by the 15th Day of the fifth month after the end of your annual accounting period.

Processing of income tax returns and assessments of any taxes due will not be delayed should a petition for declaratory judgment be filed under section 7428 of the Code.

We will make this letter and the proposed adverse determination letter available for public inspection under Code section 6110 after deleting certain identifying information. We have provided to you, in a separate mailing, Notice 437, Notice of Intention to Disclose. Please review the Notice 437 and the documents attached that show our proposed deletions. If you disagree with our proposed deletions, follow the instructions in Notice 437.

If you decide to contest this determination, you may file an action for declaratory judgment under the provisions of section 7428 of the Code in one of the following three venues: 1) United States Tax Court, 2) the United States Court of Federal Claims, or 3) the United States District Court for the District of Columbia. A petition or complaint in one of these three courts must be filed within 90 days from the date this determination letter was mailed to you. Please contact the clerk of the appropriate court for rules for filing petitions for declaratory judgment. To secure a petition form from the United States Tax Court, write to the United States Tax Court, 400 Second Street, N.W., Washington, D.C. 20217. See also Publication 892.

You also have the right to contact the office of the Taxpayer Advocate. Taxpayer Advocate assistance is not a substitute for established IRS procedures, such as the formal appeals process. The Taxpayer Advocate cannot reverse a legally correct tax determination, or extend the time fixed by law that you have to file a petition in a United States Court. The Taxpayer Advocate can however, see that a tax matters that may not have been resolved through normal channels get prompt and proper handling. If you want Taxpayer Advocate assistance, please contact the Taxpayer Advocate for the IRS office that issued this letter. You may call toll-free, 1-877-777-4778, for the Taxpayer Advocate or visit www.irs.gov/advocate for more information.

If you have any questions, please contact the person whose name and telephone number are shown in the heading of this letter.

Sincerely Yours,

Appeals Team Manager

Enclosure:

Publication 892 and/or 556

* * * * *

Dear * * *:

We have considered your application for recognition of exemption from federal income tax under Internal Revenue Code section 501(a). Based on the information provided, we have concluded that you do not qualify for exemption under Code section 501(c)(3). The basis for our conclusion is set forth below.

ISSUES

Do you meet the operational test under section 501(c)(3) of the Code? No, for the reasons set forth below.

FACTS

D, your founder, is a Certified Body Talk Practitioner, Animal Talk Practitioner, Fuji-San Practitioner, Complete Mind and Body Instructor and Hypnotherapist. She is also a Breakthrough Facilitator for Body Talk and a Reiki Master.

About 7 years ago, D worked with a local animal rescue organization in B, doing healing sessions with its dogs. In that same year, D provided healing services to an animal rescue in an African country providing such services to all types of animals. D saw that her healing sessions had successful results. When D returned to the US the next year, she formally started a sole proprietorship to provide healing sessions to animals in distress. Media sources started to interview D and she was asked to speak and teach at local health functions. A website was developed to market the proprietorship's services and its services were being requested by various animal rescues around the world. The sole proprietorship also worked private clients for a fee to fund the expenses related to providing services to the animal rescues. The income and expenses from the sole proprietorship were reported on D's personal taxes as business income and for the past few years it operated at a loss of between $8000 and $15,000. Because opportunities for funding through donations and sponsorships began to present themselves, D incorporated you as a non-profit corporation under the state law of B on date C to conduct the same services as provided by the sole proprietorship.

Your Articles of Incorporation indicate your purpose is "to work with animals and people in their natural habitat, to support balance [to] those who have experienced trauma in their environment or through their experiences, by facilitating the best possible outcome for the individual and everyone involved, based on universal energy laws that entail a holistic approach, while promoting self-awareness through healing and education".

Your governing body consists of D, who acts as President and Executive Director, a Treasurer/Operations Manager, a Secretary and 2 other board members.

- Your treasurer owns a doggie day care and pet training facility.

- Your secretary is a licensed cosmetologist, touring musician, and creator of a custom line of jewelry. She is also a motivational speaker for recovering addicts.

- Board member #1 is a certified yoga practitioner and a flower essence practitioner as well as a long time devotee of natural healing remedies.

- Board member #2 is a singer/song writer.

Your programs are essentially the same as those of the sole-proprietorship as described below:

1. You will provide healing services for individuals and their pets for a suggested donation of v dollars, which is the amount the sole proprietorship charged. You will only provide healing services to those individuals who make the suggested donation of v dollars, which is the low-end fee amount typically charged for such sessions in your city. These services consist of individual tailored sessions catered toward each client's individual needs. The client is required to complete an intake sheet for the animal receiving treatment. Healing services may involve Body Talk, CCMBA, Reiki, clairvoyant readings, past-life regression therapy, Fuji-san, Etheric Plane Communication, Multi-Generational Healing, channeling and numerology. The main goal of these sessions is to support the client in the awakening experience and bring the client back to balance and wholeness. You provided a detailed intake sheet concerning clients' pets that are being treated. By signing the intake sheet, the client agrees to pay the "suggested donation" and agrees that a 24 hour cancellation notice is required to avoid any charges for the scheduled session. There will be about 10 sessions per week for about 10 months of the year. D will be paid about w dollars per session.

2. You will provide free healing services for animal rescue organizations. D "specializes" in releasing the traumas in the animals being rescued. She also works with the rescuers and their secondary traumas that occur from continued exposure to the events that have caused the traumas to these animals in the first place. There will also be two trips abroad for these services where she will offer about 20 sessions per trip and be compensated w dollars per session.

3. You will offer one or two retreats in F for individuals who wish to do deep healing work for themselves through alternate modalities that are used to bring their mind, body, and spirit back into balance. Individuals will be requested to make a reasonable donation of x dollars. You will also offer the same retreats for individuals in the animal rescue world for no charge. These retreats will have five facilitators with D as the primary facilitator. She will organize all events and activities and will be paid v dollars per person per day. The facilitators will receive about $1000 and their expenses will be paid. Board member #1 is also a facilitator.

You only provided general itineraries as follows:

Day 1 -- Fly to F.

Yoga and Breath work with facilitator

Lunch and Dinner

Day 2 -- Meditation with facilitator

Breakthrough Facilitation with facilitator

Breakfast, Lunch and Dinner

Day 3 -- Breath work with facilitator

Healing Past, Present and Multi-Generational Traumas

Breakfast, Lunch, and Dinner

Day 4 -- Yoga with facilitator

Intimate Communications with volunteer

Breakfast, Lunch and Dinner

Day 5 -- Meditation with facilitator

Dolphin Journey and Blessing

Breakfast, Lunch and Dinner

Day 6 -- Return home.

4. You will host workshops and seminars to empower others to do the kind of healing work that you do. Topics may include animal communication workshops and Egyptian Numerology workshops. These workshops will be provided to the nonprofit animal rescue world free of charge while you will provide them to the public for a fee. D will conduct the workshops and there will be a maximum of ten participants. She will receive w dollars per person participating in the workshop with a maximum of 10 participants.

5. You will conduct various outreach activities to promote your work. D will be responsible for conducting these outreach activities. Furthermore, she will design, produce, and market advertising and internet materials. She will also develop and maintain media relations for guest appearances as well as organize and hosts booths at trade shows.

Based on the activities described above, D's compensation will be about y dollars. In addition, you have no limits set on the compensation that D can earn.

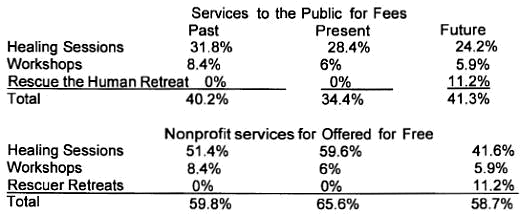

The percentage breakdown of your activities is described below:

You are using the same website as the sole-proprietorship which promotes and describes your services. There are also testimonials from satisfied clients consisting of both individuals and animal rescue organizations.

In addition, the website sells a book in which D is one of several authors. You buy the book at cost and charge ten dollars above cost; these proceeds are then donated to you. Moreover, there is a link to a website selling unique antique jewelry operated by another business D owns. Twenty five percent of these proceeds is returned to you and another twenty five percent is donated to an animal rescue while the remainder is for D's business.

You indicated your marketing strategy is to sell your programs to animal rescuers worldwide. This will be accomplished by creating and maintaining a network of contacts that will serve as a referral source for your programs. Moreover, you will develop your public image and your recognition through good public relations with your current relationships, outreach programs, education programs, and word of mouth. You will continue to engage various forms of media to cover your operations, such as newspapers, trade publications, social media, and radio and television interviews. Your brochures have been developed to sell the benefits of your programs to both potential referrers, and participants. The ultimate goal will be to build an effective marketing program, based on the success of the relationships you have already developed and to further it with future relationships you will mentor. Finally, the core of your marketing strategy will be the creation of your board of directors who will be chartered with the responsibility of selling the benefits of the program to the community.

Other than D, the rest of the labor associated to your efforts is voluntary. Your revenue is a mix offers for services (Suggested donations), and gifts, grants and contributions. Currently, your main expenses are for the salary of D, the cost of educational materials, animal supplies and travel.

Finally, you indicated there are no written contracts concerning your relationships with other entities (animal rescues and the like). All charitable work being done with animal rescues has been in the form of verbal permission and consent. All other services have come in the form of verbal discussions only. These entities and individuals are awaiting your tax exempt determination before any written contracts will be considered. Moreover, you reported that most of the materials used during your workshops and retreats is disseminated verbally or physically demonstrated in confidence at the meetings. Printed materials and handouts provided to clients are based on a non-disclosure agreement. Thus, you provided none of these materials. You also did not provide a completed Schedule G because "it would not be in your best interest since you are technically still operating as a for profit." You will continue to pay taxes until you are granted exempt status.

LAW

Section 501(c)(3) of the Internal Revenue Code of 1986 (the "Code") provides for the exemption from federal income tax of corporations organized and operated exclusively for charitable and educational purposes, no part of the net earnings which inures to the benefit of any private shareholder or individual.

Section 1.501(c)(3)-1(a)(1) of the Income Tax Regulations provides that in order to be exempt as an organization described in section 501(c)(3), an organization must be both organized and operated exclusively for one or more purposes specified in such section. If an organization fails to meet either the organizational test or the operational test, it is not exempt.

Section 1.501(c)(3)-1(c)(1) of the Income Tax Regulations provides that an organization operates exclusively for exempt purposes only if it engages primarily in activities that accomplish exempt purposes specified in section 501(c)(3) of the Code. An organization must not engage in substantial activities that fail to further an exempt purpose.

Section 1.501(c)(3)-1(c)(2) of the Income Tax Regulations provides that an organization is not operated exclusively for one or more exempt purposes if its net earnings inure in whole or in part to the benefit of private shareholders or individuals as defined in Section 1.501(a)-1(c).

Section 1.501(c)(3)-1(d)(1)(ii) of the Income Tax Regulations provides that an exempt organization must serve a public rather than a private interest. The organization must demonstrate that it is not organized or operated to benefit private interests such as "designated individuals, the creator or his family, shareholders of the organization, or persons controlled, directly or indirectly, by such private interests." Thus, if an organization is operated to benefit private interests rather than for public purposes, or is operated so that there is prohibited inurement of earnings to the benefit of private shareholders or individuals, it may not retain its exempt status.

In Revenue Ruling 77-366, 1977-2 C.B. 192, a nonprofit organization that arranged and conducted winter-time cruises during which activities to further religious and educational purposes were provided in addition to extensive social and recreational activities was not operated exclusively for exempt purposes and did not qualify for exemption.

In Revenue Ruling 77-430, 1977-2 C.B. 194, an otherwise qualifying organization that conducted weekend religious retreats, open to individuals of diverse Christian denominations, at a rural lakeshore site at which the participants may enjoy the recreational facilities in their limited amount of free time and that, charged no fees is operated exclusively for religious purposes and qualifies for exemption.

In Better Business Bureau of Washington D.C., Inc. v. United States, 326 U.S. 279 (1945), the Supreme Court held that the presence of a single non-exempt purpose, if substantial in nature, will destroy the exemption regardless of the number or importance of truly exempt purposes. The Court found that the trade association had an "underlying commercial motive" that distinguished its educational program from that carried out by a university.

In Harding Hospital, Inc. v. United States, 505 F.2d 1068 (6th Cir. 1974), the court held that an organization seeking a ruling as to recognition of its tax-exempt status has the burden of proving that it satisfies the requirements of the particular exemption statute.

In Airlie Foundation v. Commissioner, 283 F. Supp. 2d 58 (D.D.C., 2003), the court relied on the "commerciality" doctrine in applying the operational test under section 501(c)(3). Because of the commercial manner in which the organization conducted its activities, the court found that it was operated for a non-exempt commercial purpose, rather than for a tax-exempt purpose. The case noted that among the major factors that courts have considered in assessing commerciality are competition with for-profit entities, pricing policies, the extent and degree of below cost services provided and the reasonableness of financial reserves. Additional factors include whether the organization uses commercial promotional methods (such as advertising) and the extent to which the organization receives charitable donations.

In Asmark Institute. Inc. v. Comm'r, 110 AFTR 2d 2012-5077 (July 3, 2012), the Tax Court found that the organization was not operated exclusively for tax exempt purposes, because "its operations were commercial rather than charitable" and because its activities "consist mainly of compliance services for a fee" which competed with commercial businesses. The organization also promoted itself to expand its client base and did not provide significant free services. In addition, the organization was operated for the same purpose as its for-profit predecessor: serving as a fee-for-service consulting resource center for compliance materials and services for the agribusiness industry.

APPLICATION OF LAW

You are not as described in section 501(c)(3) of the Code because you are not exclusively operated for charitable or educational purposes.

You are not as described in Section 1.501(c)(3)-1(a)(1) of the Regulations because you fail the operational test.

You do not meet the provisions in Section 1.501(c)(3)-1(c)(1) of the regulations because you are operating for substantial non-exempt purposes. You are operating for private purposes as evidenced by the fact you took over D's sole proprietorship that was. operating at a loss to conduct the same activities. You are operating for substantial commercial purposes as indicated by the fact that a substantial portion of your activities is providing services tailored to the specific needs of each client for a fee. Your marketing strategy of selling your services worldwide also illustrates you are operating for a substantial commercial purpose.

As described in section 1.501(c)(3)-1(c)(2) of the Regulations, you are not operated exclusively for exempt purposes because your net earnings inure to the benefit of D. For example:

- You were formed by D to obtain grant money to provide the same services as her sole-proprietorship, which has been operating at a loss for the last several years;

- The fact that D who is your incorporator, your executive director, your president and your only paid employee is in complete control of your operations. Further, there is no upper limit to the amount of compensation she can earn;

- There is a link on the website to D's for profit jewelry business. Even though some of the proceeds are being donated to you and another animal rescue, D receives a substantial benefit;

- You are also selling a book on your website for ten dollars above cost in which D is one of the authors. Even though the proceeds are being donated to you and another animal rescue, D is receiving a benefit from each sale.

You are not as defined in Section 1.501(c)(3)-1(d)(1)(ii) of the Regulations because you are operating to confer the advantages of tax-exempt status to D as shown by the fact that your tax exemption will enable her to apply for grants to continue her business that has been operating at a loss. You are also operating for the private interests of your board members because they have related businesses and are in a favorable position to benefit from your operations.

You are similar to the organization described in Revenue Ruling 69-266 because your primary function is to benefit your founder. This is illustrated by the fact you took over her business which was operating at a loss and are providing the exact same services conducted by D for the same prevailing fees and consequently, your operations do not differ significantly from D's sole proprietorship. Therefore, you are operating for private interests.

Your retreats are not like those described in Rev. Rul. 77-430, 1977-2 CB 194 because they serve a non-exempt recreational purpose as evidenced by the itinerary and the location of the retreats. Your retreats are like those of the organization in Rev. Rul. 77-366, 1977-2 CB 192. Even if some of the activities are educational in nature, there is substantial time available for recreational and other non-exempt activities. Thus, the retreats do not meet the requirements of Section 501(c)(3).

You are similar to Bubbling Well Church of Universal Love, Inc. v. Commissioner. You have not provided an open candid disclosure of facts. You have given answers to our inquiries that were vague, and uninformative. For example, you

- Did not provide Schedule G because it "would not be in your best interest since you are technically still operating as a for profit."

- Provided only general itineraries for your retreats.

- Did not provide literature because of your non-disclosure policies.

You are like the organization in Better Business Bureau v. Commissioner. Although you may have some educational purposes, the presence of non-exempt private purposes precludes exemption under section 501(c)(3).

Similar to the organization in Harding Hospital, Inc. v. United States, you have the burden of proving that you satisfy the requirements for tax exemption. You have failed to prove that you are not operating for the benefit of D and for substantial non-exempt purposes.

You are similar to the organization in Airlie Foundation v. Commissioner. You are taking over the operations of D's sole-proprietorship and there is little indication that your operations have changed. For example, D remains your only employee and you provide the same healing services for the same fees as you did as a sole proprietorship. Your marketing strategy "to sell your programs to animal rescuers worldwide" is characteristic of a for profit business. The fact that your printed materials and handouts provided to clients are based on a non-disclosure agreement is also indicative of a for profit business. In addition, the fact your intake sheet requires the client to pay the "suggested donation" and agrees that a 24 hour cancellation notice is required to avoid any charges for the scheduled session indicates you have a commercial purpose. Finally, the fact that you have testimonials on your website from satisfied clients is a common technique used by for profit businesses.

Your operations are similar to those of the organization described in the court case Asmark. Like this organization, you took over your founder's for profit business, a substantial portion of your services is provided for a fee in the same manner as your predecessor, you have an aggressive marketing strategy to expand your business model and you are staffed like your predecessor. Consequently, you are operating for a substantial commercial purpose which disqualifies you from exemption.

APPLICANT'S POSITION

You wrote, you are aware that while you await your nonprofit status, you are still considered a for-profit corporation. You will continue to pay income taxes until you receive a determination on your tax-exempt status. You are seeking nonprofit status in order to attract donors who wish to make tax-deductible contributions and to be eligible for funding from governmental and charitable sources. Since you are not technically a nonprofit, you did not feel it was in your best interest to provide information on your succession from the sole proprietorship to your current form.

You report that the animal organizations that you have aligned with have seen much benefit from the healing work you provide. Countless case studies, with before and after photos and testimonials give you further confirmation that your mission is being fulfilled. Your only obstacle is your need for more financial backing. With your nonprofit status being confirmed, you could qualify for grants and sponsorships. This would allow you to work with organizations that you previously had to turn away. You respectfully request exempt status.

SERVICE RESPONSE TO APPLICANT'S POSITION

You failed to provide any additional information from which it can be concluded that your activities exclusively further or advance a purpose described in Section 501(c)(3). Although you have provided information on your programs and how you feel they meet the standard of tax exemption, you have not demonstrated how your operations exclusively further an exempt purpose. Further, the details as analyzed previously, show you are serving substantial commercial and private purposes.

CONCLUSION

Based on the facts, we conclude that you are not in compliance with the above stated laws and precedence. The details that you have provided do not demonstrate how you meet the operational test under section 501(c)(3) of the Code. Further, there is evidence of substantial non-exempt purposes. Accordingly, you do not qualify for exemption as an organization described in Section 501(c)(3) of the Code and you must file federal income tax returns. Contributions to you are not deductible under Section 170.

You have the right to file a protest if you believe this determination is incorrect. To protest, you must submit a protest statement explaining your views and reasoning. You must submit the protest statement, signed by one of your officers, within 30 days from the date of this letter. We will consider your statement and decide if the information affects our determination. If your protest statement does not provide a basis to reconsider our determination, we will forward your case to our Appeals Office. You can find more information about the role of the Appeals Office in Publication 892.

Types of information that should be included in your protest statement can be found in Publication 892. The protest statement must be accompanied by the following declaration:

"Under penalties of perjury, I declare that I have examined this protest statement, including accompanying documents and to the best of my knowledge and belief, the statement contains all relevant facts and such facts are true, correct, and complete."

Your protest will be considered incomplete without this statement.

If an organization's representative submits the protest, a substitute declaration must be included stating that the representative prepared the protest and accompanying documents; and whether the representative knows personally that the statements of facts contained in the protest and accompanying documents are true and correct.

An attorney, certified public accountant, or an individual enrolled to practice before the Internal Revenue Service may represent you during the appeal process. If you want representation during the appeal process, you must file a proper power of attorney, Form 2848, Power of Attorney and Declaration of Representative, if you have not already done so. You can find more information about representation in Publication 947, Practice Before the IRS and Power of Attorney. All forms and publications mentioned in this letter can be found at www.irs.gov, Forms and Publications.

If you do not file a protest within 30 days, you will not be able to file a suit for declaratory judgment in court because the Internal Revenue Service (IRS) will consider the failure to appeal as a failure to exhaust available administrative remedies. Code Section 7428(b)(2) provides, in part, that a declaratory judgment or decree shall not be issued in any proceeding unless the Tax Court, the United States Court of Federal Claims, or the District Court of the United States for the District of Columbia determines that the organization involved has exhausted all of the administrative remedies available to it within the IRS.

If you do not intend to protest this determination, you do not need to take any further action. If we do not hear from you within 30 days, we will issue a final adverse determination letter. That letter will provide information about filing tax returns and other matters.

Please send your protest statement, Form 2848, and any supporting documents to the applicable address:

Mail to:

Internal Revenue Service

EO Determinations Quality Assurance

Room 7-008

P.O. Box 2508

Cincinnati, OH 45201

Deliver to:

Internal Revenue Service

EO Determinations Quality Assurance

550 Main Street, Room 7-008

Cincinnati, OH 45202

You may fax your statement using the fax number shown in the heading of this letter. If you fax your statement, please call the person identified in the heading of this letter to confirm that he or she received your fax.

If you have any questions, please contact the person whose name and telephone number are shown in the heading of this letter.

Sincerely,

Tamera Ripperda

Director, Exempt Organizations

Enclosure:

Publication 892