Private Letter Rulings - Org Promoting Economic Revitalization Loses Exemption

GiftLaw Note:

Organization was formed as a 501(c)(3) for the purposes of promoting social welfare of City and the areas around City by encouraging business development likely to benefit low income people. Organization’s bylaws stated that it also sought to secure financing to build or rent a facility to house companies that could aid in business development. Organization owns a commercial building that it rents at below market rates to the public. The building is debt-financed with acquisition indebtedness. During a recent 12-month period, Organization hosted two online one-day seminars on QuickBooks and social media marketing. Organization’s President indicated that it does not have the capacity to conduct an extensive level of charitable or educational activities.

Tax exempt organizations under Sec. 501(c)(3) must be both organized and operated exclusively for exempt purposes. Here, while the Service found that Organization’s bylaws established it was organized for exempt purposes, it was not being operated for such purposes. First, Organization’s only recent exempt activity was conducting two online seminars on QuickBooks and social media. Second, Organization was not pursuing its stated purpose of promoting economic revitalization in an economically depressed area. Organization’s commercial building is not located in a depressed area and City’s job market and employment growth are strong. Finally, all of Organization’s resources went to managing the commercial building and rental activities, none of which was furthering exempt purposes. Organization rents office space to anyone that can afford it regardless of whether the tenant is in a charitable class or would engage in activities designed to help a charitable class. In addition, the commercial building is debt-financed property and the rental activity is an unrelated trade or business under Sec. 513(a). Therefore, the IRS revoked Organization’s tax-exempt status under Sec. 501(c)(3).

Tax exempt organizations under Sec. 501(c)(3) must be both organized and operated exclusively for exempt purposes. Here, while the Service found that Organization’s bylaws established it was organized for exempt purposes, it was not being operated for such purposes. First, Organization’s only recent exempt activity was conducting two online seminars on QuickBooks and social media. Second, Organization was not pursuing its stated purpose of promoting economic revitalization in an economically depressed area. Organization’s commercial building is not located in a depressed area and City’s job market and employment growth are strong. Finally, all of Organization’s resources went to managing the commercial building and rental activities, none of which was furthering exempt purposes. Organization rents office space to anyone that can afford it regardless of whether the tenant is in a charitable class or would engage in activities designed to help a charitable class. In addition, the commercial building is debt-financed property and the rental activity is an unrelated trade or business under Sec. 513(a). Therefore, the IRS revoked Organization’s tax-exempt status under Sec. 501(c)(3).

5/27/2016 (3/4/2016)

Dear * * *:

* * * *

ISSUE

Whether ORG ("ORG") was operated exclusively for charitable or educational purposes within the meaning of Internal Revenue Code ("IRC") section 501(c)(3).

FACTS

ORG incorporated on January 28, 19XX in State and is currently in active status according to the State State Secretary of State.

ORG states that it is currently in the process of dissolving but has not filed articles of dissolution with the State of State nor a final return tax return with the IRS.

Per the Articles of Incorporation, ORG is organized exclusively for charitable and educational purposes within the meaning of IRC section 501(c)(3). ORG's purpose is to promote social welfare of City and City by fostering business development likely to benefit low and moderate-income people in the City and City areas.

With Form 1023 dated November 30, 19XX, ORG applied for exemption under IRC section 501(c)(3) to:

1. Create new jobs, promote business growth, and promote economic revitalization in the economically depressed area of City, State,

2. Provide access for small businesses to financing and business consulting,

3. Target businesses that create employment opportunities for low to moderate income families, especially minority and women-owned businesses,

4. Acquire a building and rent low-cost space to small businesses and entrepreneurs,

5. Provide low cost on-site management services,

The IRS issued Letter 1050 in October 19XX recognizing ORG as an exempt organization described in IRC section 501(c)(3) and a public charity described in Code section 170(b)(1)(A)(vi).

Per its amended bylaws, adopted on March 3, 19XX, ORG is to:

1. Promote social welfare by fostering business development, providing financial and managerial services, providing educational and technical services to enhance the survival and development of entrepreneurship and businesses likely to benefit low and moderate income people,

2. Organize and manage a small business incubator,

3. Secure financing to build or rent a facility to house companies, which may seek to do business within this incubator.

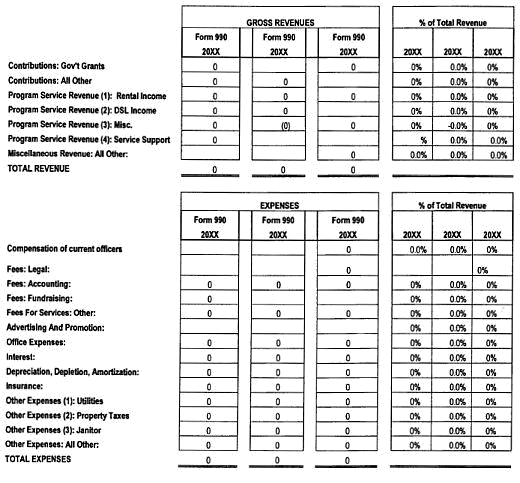

The following table compares ORG's revenues and expenses reported on the Form 990's under examination and shows the organization incurred a loss in each year.

ORG owns a 0 sq. ft. commercial office building and an adjacent parking lot located at Address, City, State that is debt-financed with acquisition indebtedness. The commercial building has approximately 0 offices and cubicles available to rent at below market rates by the public.

ORG's tenant selection process consists of:

1. Completing a standard lease obtained from the American Industrial Real Estate Association

2. Providing rental history, employment history, credit info,

3. Providing a brief description of their business.

ORG's largest tenants from July 1, 20XX to June 30, 20XX, were:

- Law Offices (6),

- Marketing Firms and Special Event Staffing (5),

- Exempt Organizations (3),

- Real Estate (2),

- Financial Service Providers (2),

- Hospice and Assisted Living Providers (2),

- Communication Businesses (2)

During the 12-month period ended June 30, 20XX, ORG offered two online one-day seminars on QuickBooks and using social media for marketing. The President stated ORG did not have the capacity to conduct an extensive amount of charitable or educational activities.

ORG's day-to-day operations and property management activities were performed by:

1. Volunteers, and

2. Independent contractors

LAW

Code section 501(c)(3) provides exemption from federal income taxes of organizations organized and operated exclusively for charitable and educational purposes. . . .

Code section 511(a)(1) imposes a tax on the unrelated business taxable income of organizations described in section 501(c).

Code section 512(a)(1) defines the term "unrelated business taxable income" as the gross income derived by any organization from any unrelated trade or business regularly carried on by it, less allowable deductions which are directly connected with the carrying on of such trade or business.

Code section 512(b) provides that all rents from real property are excluded from the term "unrelated business taxable income" except in the case of amounts derived from debt-financed property (as defined in section 514).

Code section 513(a) provides that the term "unrelated trade or business" means any trade or business the conduct of which is not substantially related (aside from the need of such organization for income or funds or the use it makes of the profits derived) to the exercise or performance by such organization of its charitable, educational, or other purpose or function constituting the basis for its exemption under section 501.

Code section 514(b)(1) defines "debt-financed property" as any property that is held to produce income and with respect to which there is an acquisition indebtedness at any time during the taxable year.

Code section 514(b)(1)(A)(i) provides that the term "debt-financed property" does not include any property substantially all the use of which is substantially related (aside from the need of an organization for income or funds) to the exercise or performance by such organization of its charitable, educational, or other purpose or function constituting the basis for its exemption.

Regulation section 1.501(c)(3)-1(a) states that in order to be exempt as an organization described in section 501(c)(3), an organization must be both organized and operated exclusively for one or more of the purposes specified in such section. If an organization fails to meet either the organizational test or the operational test, it is not exempt.

Regulation section 1.501(c)(3)-1(b) Organizational test -- (1) In general. (i) An organization is organized exclusively for one or more exempt purposes only if its articles of organization:

(a) Limit the purposes of such organization to one or more exempt purposes; and

(b) Do not expressly empower the organization to engage, otherwise than as an insubstantial part of its activities, in activities, which in themselves are not in furtherance of one or more exempt purposes.

Regulation section 1.501(c)(3)-1(c) Operational test -- (1) Primary activities. An organization will be regarded as operated exclusively for one or more exempt purposes only if it engages primarily in activities which accomplish one or more of such exempt purposes specified in section 501(c)(3). An organization will not be so regarded if more than an insubstantial part of its activities is not in furtherance of an exempt purpose.

Regulation section 1.501-(c)(3)-1(d)(i) Exempt purposes -- An organization may be exempt as an organization described in section 501(c)(3) if it is organized and operated exclusively for purposes such as:

(a) Charitable,

(b) Educational

Regulation section 1.501(c)(3)-1(d)(ii) provides an organization is not organized or operated exclusively for one or more of the purposes specified in subdivision (i) of this subparagraph unless it serves a public rather than a private interest.

Regulation section 1.501(c)(3)-1(d)(2) provides that the term "charitable" is used in section 501(c)(3) of the Code in its generally accepted legal sense. The term includes: relief of the poor and distressed or of the underprivileged; lessening of the burdens of Government; and promotion of social welfare. The Service has long held that poor and distressed beneficiaries must be needy in the sense that they cannot afford the necessities of life. See Rev. Proc. 96-32, 1996-1 C.B. 717, section 2.01

Regulation section 1.501(c)(3)-1(d)(3) provides that the term "educational" refers to: (a) The instruction or training of the individual for the purpose of improving or developing his capabilities; or (b) The instruction of the public on subjects useful to the individual and beneficial to the community.

Regulation section 1.501(c)(3)-1(e)(1) provides that an organization may meet the requirements of section 501(c)(3) although it operates a trade or business as a substantial part of its activities, if the operation of such trade or business is in furtherance of the organization's exempt purpose or purposes and if the organization is not organized or operated for the primary purposes of carrying on an unrelated trade or business. In determining the existence or nonexistence of such primary purpose, all the circumstances must be considered, including the size and extent of the trade or business and the size and extent of the activities which are in furtherance of one or more exempt purposes. An organization which is organized and operated for the primary purpose of carrying on an unrelated trade or business is not exempt under section 501(c)(3).

In Revenue Ruling 76-419, 1976-2 C.B. 146, a nonprofit organization was formed with the objectives of the relief of poverty, dependency, chronic unemployment, and underemployment, and the reduction of community tensions in an economically depressed community. In furtherance of these purposes the organization encouraged industrial enterprises to locate new facilities in the economically depressed area in order to provide more employment opportunities for low-income residents. The organization purchased blighted land in the depressed area and converted it into an industrial park. Lots in the industrial park were leased to industrial enterprises on terms sufficiently favorable to attract tenants to the area. Tenants were required by their lease with the organization to hire a significant number of presently unemployed persons in the area and to train them in needed skills. The organization in selecting tenants for the industrial park, considered only those industrial enterprises whose hiring policies conformed to current fair employment law. Enterprises that had initial requirements for low skill workers were favored over those with initial high skill job requirements, since the former were of greater immediate benefit to the surrounding depressed community. The area in which the organization was active had been identified by governmental authorities as having a high ratio of unemployed and underemployed low-income people.

In Better Business Bureau of Washington D.C., Inc. v. United States, 326 U.S. 279 (1945), the Supreme Court held that the presence of a single non-exempt purpose, if substantial in nature, will destroy the exemption regardless of the number or importance of truly exempt purposes. The Court found that the trade association had an "underlying commercial motive" that distinguished its educational program from that carried out by a university.

In B.S.W. Group. Inc. v. Commissioner, 70 T.C. 352, 357-358 (1978), the Tax Court held that when considering whether an organization qualifies for exemption under section 501(c)(3) the critical inquiry is whether petitioner's primary purpose for engaging in its sole activity is an exempt purpose, or whether its primary purpose is the nonexempt one of operating a commercial business producing net profits for petitioner. Factors such as the particular manner in which an organization's activities are conducted, the commercial hue of those activities, and the existence and amount of annual or accumulated profits are relevant evidence of a forbidden predominant purpose.

GOVERNMENT'S POSITION

An organization may be held exempt only if its primary purpose is to engage in the type of activity prescribed in the Code section under which it claims exemption. If it is found that an organization's primary purpose is the conduct of a business of a type ordinarily carried on for profit, and not the furtherance of an exempt purpose, exemption cannot be established.

ORG's Articles of Incorporation, Form 1023, and Amended Bylaws establish it was organized for charitable and educational purposes:

1. Promoting economic revitalization in an economically depressed area serves a charitable purpose and benefits a charitable class of people.

2. Creating employment opportunities for the poor, distressed, or underprivileged serves a charitable purpose and benefits a charitable class of people.

3. Offering seminars and technical training to entrepreneurs serves an educational purpose

Based on the interview of ORG's President and the examination of operational and financial records it cannot be established ORG was operated for charitable and educational purposes because the organization only carried out a marginal amount of activities that further an exempt purpose. The only educational activities conducted during the year ended June 30, 20XX were two seminars on QuickBooks and social media. ORG did not provide any financial assistance to small businesses or non-profits as stated in the Articles of Incorporation.

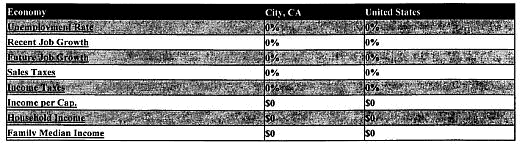

There is no evidence ORG promoted economic revitalization in an economically depressed. ORG's commercial building was not located in a blighted area as described in Revenue Ruling 76-419. Per www.bestplaces.net, City, State has maintained a strong job market and employment growth compared to the rest of the United States.

All of ORG's resources were devoted to managing the building and rental activities. From July 1, 20XX to June 30, 20XX, 0% of ORG's gross revenues were from rental income.

From July 1, 20XX to June 30, 20XX, there was an insubstantial amount of expenditures that furthered an exempt purpose:

- 0% of ORG's gross expenses were related to interest for the building and parking lot,

- 0% of ORG's gross expenses were depreciation,

- 0% of ORG's gross expenses were utilities,

- 0% of ORG's gross expenses were property taxes,

- 0% of ORG's gross expenses were related to janitorial services

ORG contracted a property manager to execute leases, collect rent, manage the building, and oversee major repairs. The property manager did not have a criteria used to select tenants. ORG provided office space to anyone that could afford it without any consideration given to whether the tenant was in a charitable class or would provide relief to a charitable class. Renting office space to the public does not further an exempt purpose.

Because the building is debt-financed property" as defined by Code section 514(b)(1), the rental activity is an unrelated trade or business as provided by Code section 513(a).

Based on the fact that the majority of resources used by ORG are related to the rental activities, and the absence of activities which further an exempt purpose, ORG fails the operational test provided in § 1.501(c)(3)-1(c)(1) of the Regulations and is not entitled to exemption under § 501(c)(3) of the Code. Similarly to Better Business Bureau of Washington D.C., Inc. v. United States. 326 U.S. 279 (1945), the presence of a single non-exempt purpose, substantial in nature, disqualifies the organization from exemption.

TAXPAYER'S POSITION

The Assigned Agent presented the facts, law, and government's position to the taxpayer and is awaiting their response.

CONCLUSION

ORG's primary purpose was to maintain a commercial office building and rent office space to the public. The tenants were not a charitable class of individuals and renting office space at below market rates did not serve an exempt purpose. ORG was not operated exclusively for charitable or educational purposes within the meaning of IRC section 501(c)(3).

Accordingly, ORG's exempt status should be revoked effective July 1, 20XX. Contributions will no longer be deductible under section 170 of the Internal Revenue Code. Form 1120 returns should be filed for all tax periods ending on or after June 30, 20XX.